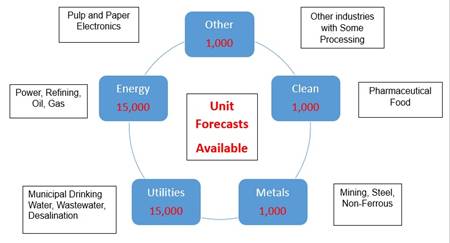

DETAILED FORECASTING OF MARKETS, PROSPECTS AND PROJECTS

It is now possible to precisely segment and predict markets, identify the

prospects, and track the most important projects.

A few hundred companies make most of the flow control and treatment purchasing

decisions. McIlvaine is identifying them and reporting on their

activities.

Detailed forecasting of markets, prospects and projects provides the following

benefits:

Improve decisions on allocation of direct sales, promotion and development

expenditures

Increase orders cost effectively

Review strategy with better insights as to improvement

Find out the details with:

This Year 133 Companies Will Buy 55 Percent of the Fabric Filters

Purchases of fabric filter systems will exceed $8 billion in 2015. One hundred

thirty-three companies will account for more than $4 billion in purchases.

Steel, stone and power industries comprise two-thirds of the entire market.

These three industries are relatively consolidated, so by tracking the

activities of the major producers, the supplier reaches the majority of the

market.

The following chart shows purchases by individual companies and groups. The list

is ranked by 2015 contribution to purchases. The largest individual purchaser is

Eskom with 10 percent of the system purchases.

|

Fabric Filter Purchases 2015 |

|||

|

Company |

% of 2015

Fabric Filter Market |

Application |

% High Temp |

|

50 Power Companies with 2015

Purchases |

20 |

Coal-fired |

90 |

|

Eskom |

10 |

Coal-fired |

90 |

|

Cement Companies, ranked 7-50 |

5 |

Cement |

60 |

|

Top 10 Mining Companies in 2015 |

4 |

Mining |

60 |

|

Top 10 Chemical Companies in

2015 |

4 |

Chemical |

40 |

|

Steel Companies, ranked 2-6 |

3.3 |

Steel |

60 |

|

Top 10 WTE in 2015 |

3 |

WTE |

95 |

|

Arcelor Mittal |

1.3 |

Steel, Coal-fired

Iron Ore |

50 |

|

Lafarge |

1.2 |

Cement |

60 |

|

Holcim |

1.2 |

Cement |

60 |

|

CNEM |

1.2 |

Cement |

60 |

|

Anhui Conch |

1.2 |

Cement |

60 |

|

Total (133 Companies) |

55.1 |

60 |

|

The cement industry accounts for over 20 percent of fabric filter purchases. The

2014 production was 4.2 billion tons. Lafarge accounted for 5 percent of the

total production. Lafarge accounts for 1.25 percent of the total fabric filter

purchases. Holcim, CNBM and Ahui Conch each purchase more than 1 percent of the

collectors and bags.

World crude steel production reached 1,662 million tons (Mt) for the year 2014,

up by 1.2 percent compared to 2013.

Arcelor Mittal produced 6 percent of the total, whereas the next eight companies

average 3 percent each.

ArcelorMittal purchases a high percentage of the total fabric filters because of

its involvement in several industries. It has both iron ore and metallurgical

coal reserves and is among the largest iron ore producers in the world. Iron ore

mining operations are located in the United States, Canada, Mexico, Brazil,

Liberia, Bosnia, Ukraine, Algeria and Kazakhstan. In Canada, the company is

developing a large Greenfield project on Baffin Island. Metallurgical coal

mining operations are located in the United States and Kazakhstan.

The potential in the power industry is huge. Ninety

percent of coal-fired power plants still use precipitators. If all power plants

converted to fabric filtration, the investment would be $80 billion just for the

hardware and over $200 billion for the installed systems. The systems would

clean 8 billion cfm of flue gas and would require 4 billion square feet of

filter bags. The challenge is to determine how fast and how much capacity will

switch. The potential in China is the largest, but this year Eskom in South

Africa will be the biggest purchaser.

The large purchasers such as Arcelor Mittal are moving toward global sourcing.

One reason is to determine total cost of ownership for products and services

purchased. Individual plants without the analytical resources are forced to buy

based on lowest price. The companies who pursue these large purchasers and can

demonstrate lowest cost of ownership will boost sales and margins.

McIlvaine has a program to provide Detailed Forecasting of Markets, Prospects

and Projects for Fabric Filters. This program is built around

N021 World

Fabric Filter and Element Market,

N032

Industrial Air Plants and Projects

and

42EI Utility

Tracking System

For more information on the program contact Bob McIlvaine at

rmcilvaine@mcilvainecompany.com.

The fact that power plants in many different countries have shifted to fabric

filters is indicative of the most important development in the history of the

industry.

There is great concentration among OEMs. FLSmidth supplies a very significant

percentage of filters for their cement kiln systems. However, they make both

collectors and bags. Other kiln suppliers are major purchasers of filters. Large

power plant suppliers such as B&W and Alstom make their own collectors but buy

bags.

End Users/AEs/OEMs

The 200 largest end users, architect engineers and OEMs make 75 percent of the

decisions relative to fabric filter purchases. This is a small enough group that

detailed forecasting can be achieved at modest cost compared to the potential to

increase in sales and create greater sales efficiency.

OEM Networking Directory Has the Contacts at Consulting and Supplier Companies

If you sell systems, scrubbers nozzles, packing or corrosion resistant materials

you will use the McIlvaine OEM Networking Directory daily. Check it out

at:

53DI OEM

Networking Directory.

“Hot Topic Hour” November 12, 2015 to Focus on Latest Issues and

Innovations in Dry Scrubbing

This will be a free webinar to recommend updates to a power point presentation

of 60 slides covering a range of options and issues related to dry scrubbing.

The revised presentation and recording will be subsequently available to

McIlvaine subscribers and to any end user.

The dry scrubbing option is being taken by many operators of power plants,

incinerators, kilns and furnaces. There are many issues and innovations that

need to be addressed by decision makers. These will be summarized and discussed

in a 90 minute recorded webinar.

One of the decisions is the type of dry scrubber that is best. Originally SDA

was the main option. Now CDS is popular. DSI with the more reactive sorbents has

become an option even when higher efficiency is required. The catalytic filter

with DSI promises one stop shopping. Combinations such as DSI and SDA are also

an option.

The dry scrubber is necessarily part of a multi pollutant removal system that

addresses particulate, acid gases and toxic metals. As a result, the evaluation

of the impact of the dry scrubber on the removal pollutants such as mercury is

important. The changing regulations in the U.S., China and the EU all need to be

addressed.

Solid waste is an issue. Can the sorbent/acid/ash combination be used as

construction materials? What about

leaching of toxic metals? The loss

of flyash and gypsum revenues need to be evaluated. The benefits of lower water

use and elimination of wastewater are also important

There are many process factors. One is the sulfur content of the fuel

versus the required efficiency. Another is the temperature of the air leaving

the heat exchanger and the potential for DSI ahead of the air heater to allow

greater heat recovery.

Ten Power Generators Will Purchase 50 Percent of the Mercury Reduction Products

and Services in 2016

Mercury reduction is being accomplished by the addition of activated carbon,

bromine or other chemicals. With the new air toxic rules requiring U.S. power

plants to meet levels as low as 3 µg/m3 sales of these chemicals will

be substantial. Worldwide sales for chemicals to reduce mercury will exceed $1

billion. The electricity generator (EG) expenditures will be over $800 million.

Just ten EGs will spend an average of $40 million each and will account for over

40 percent of world purchases. Thirty-two EGs will account for 75 percent of the

purchases by EGs and 60 percent of the total mercury reduction expenditures.

|

Mercury Reduction Expenditures

for Major EGs |

|||||||

|

No. of

Corporations |

No. of FGD MW/EG

1000 |

Total

MW

1000 |

% of

Total

Installed

Base |

% of Mercury

Expenditures

Short Term |

% of

Mercury

Expenditures

Long Term |

Examples |

|

|

7 |

Over 50 |

575 |

44 |

5 |

44 |

Big 5 Chinese Corp |

|

|

10 |

10-50 |

150 |

12 |

50 |

12 |

AEP, TVA, Duke, Enel, EON |

|

|

15 |

5-10 |

105 |

8 |

20 |

8 |

NRG, Xcel, Tokyo Electric, Chubu

Electric |

|

|

20 |

3-5 |

80 |

6 |

10 |

6 |

AES, EPDC, RWE, CEZ |

|

|

52 |

Sub total |

910 |

70 |

85 |

70 |

|

|

|

350 |

0-3 |

390 |

30 |

15 |

30 |

U.S., Europe, China |

|

|

404 |

Total |

1,300 |

100 |

100 |

100 |

|

|

The U.S. is ahead of other countries in limiting mercury emissions from

electricity from EGs. However, over the next ten years, the Chinese are expected

to ratchet down emission limits to the same level as in the U.S. When this

occurs, just seven corporations will account for 44 percent of the total

purchases.

The concentration of purchasing among just a few corporations dictates a focused

effort.

McIlvaine has introduced a program incorporating detailed forecasting of total

potential sales revenue for each major prospect, project and supplier. This is

included in

N056

Mercury Air Reduction Market.

For more information contact Bob McIlvaine at

rmcilvaine@mcilvainecompany.com.

Here are some Headlines from the Utility E-Alert

§

Nederman China receives Order for Boiler Flue Gas Cleaning Project

§

Barapukuria Coal-fired Power Plant adds Third Unit

§

ABB wins Orders worth $300 Million for China Power Projects

§

China to finance Second Coal-fired Power Plant at Thar Block II

Huaneng Bayanbaolige 1,320 MW proposed Coal-fired Power Plant in Inner Mongolia

Autonomous Region, China

§

Clean Power Plan is unfolding

§

This Year 133 Companies will buy 55 Percent of Fabric Filters

§

Seventeen Power Plant Owners have Purchased 56 Percent of all the World’s FGD

Systems

§

Carbonxt and United Conveyor Corporation launch Joint Air Quality Control

Offering

§

Precipitators can compete with Fabric Filters – Hot Topic Hour Thursday October

22, 2015Upcoming Hot Topic Hours

The Utility E Alert is issued weekly and covers the coal-fired projects,

regulations and other information important to the suppliers. It is $950/yr. but

is included in the $3020 Utility Tracking System which has data on

every plant and project plus networking directories and many other features.

----------

You can register for our free McIlvaine Newsletters at:

http://www.mcilvainecompany.com/brochures/Free_Newsletter_Registration_Form.htm.

Bob McIlvaine

President

847-784-0012 ext 112

rmcilvaine@mcilvainecompany.com

www.mcilvainecompany.com